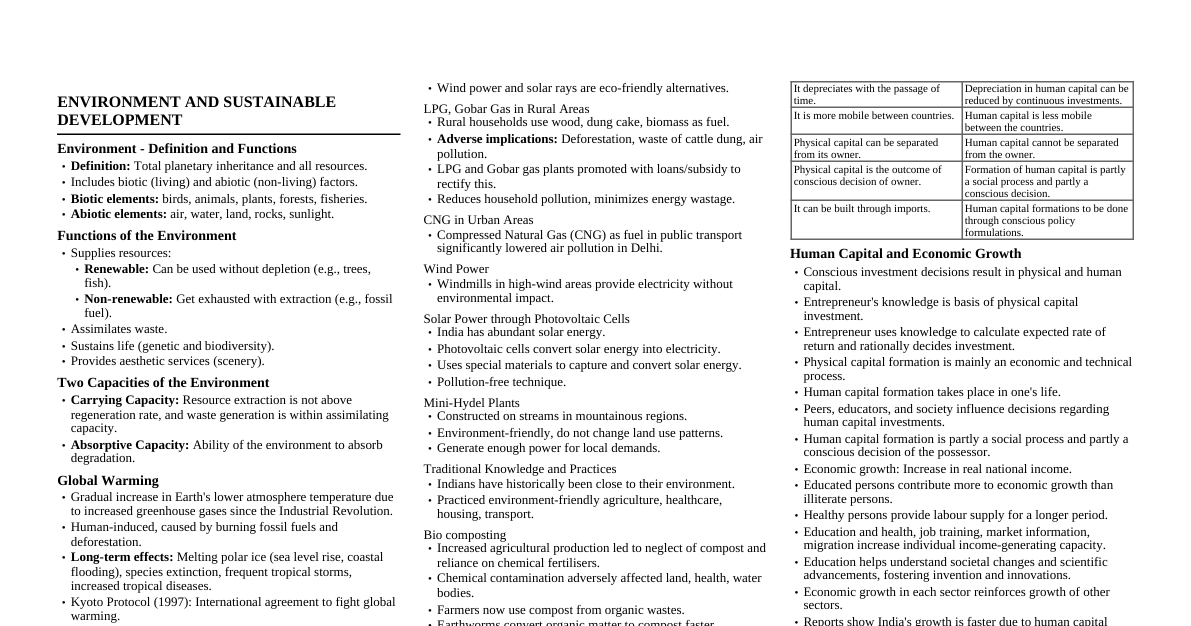

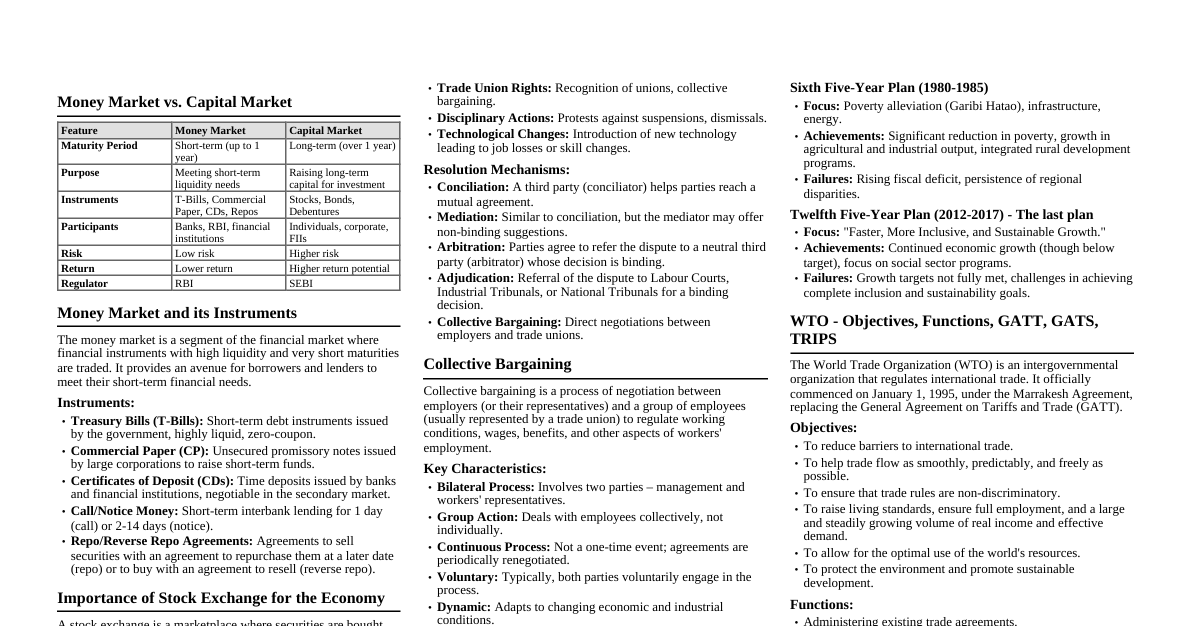

Economics for UPSC Prelims

Shared 2/11/2026•13 views

### The Study of Economics - **Microeconomics:** Focuses on individual agents (households, firms), markets, and resource allocation. Analyzes prices, output, income, and employment for specific industries or markets. - **Macroeconomics:** Deals with the economy as a whole. Studies aggregates like national income, employment, inflation, economic growth, and government policies (fiscal & monetary). ### Logic of Economics - **Positive Economics:** Describes and explains economic phenomena as they are. Deals with factual statements and can be tested or verified (e.g., "An increase in interest rates will reduce inflation"). - **Normative Economics:** Involves value judgments and prescribes what economic policies *should* be. Deals with opinions and cannot be tested (e.g., "The government *should* increase interest rates to control inflation"). ### Terms Related to Economics - **Nine Central Concepts:** 1. **Scarcity:** Unlimited wants vs. limited resources. The fundamental problem in economics. 2. **Choice:** Due to scarcity, decisions must be made about how to allocate resources. 3. **Opportunity Cost:** The value of the next best alternative foregone when a choice is made. (e.g., choosing to study means giving up leisure time). 4. **Utility:** The satisfaction or benefit derived from consuming a good or service. 5. **Goods:** Tangible items that satisfy wants. 6. **Services:** Intangible activities that satisfy wants. 7. **Factors of Production (FoP):** Resources used to produce goods and services. - **Land:** Natural resources (e.g., raw materials, energy). - **Labor:** Human effort (physical and mental). - **Capital:** Man-made resources used in production (e.g., machinery, buildings). - **Entrepreneurship:** The ability to combine FoP, innovate, and take risks. 8. **Efficiency:** Producing maximum output with minimum inputs; avoiding waste. 9. **Equity:** Fairness in the distribution of economic benefits. ### The Basic Economic Problem - **What to produce?** (What goods/services and in what quantities?) - **How to produce?** (What methods, technologies, and resources to use?) - **For whom to produce?** (How will output be distributed among the population?) ### Alternative Ways to Answer the Economic Questions - **Market Approach (Capitalism):** Economic decisions guided by supply and demand in free markets. Private ownership of FoP. Minimal government intervention. - **Command Approach (Socialism/Communism):** Economic decisions centrally planned by the government. State ownership of FoP. All resource allocation decided by central authority. - **Rationing and Economic Systems:** All economic systems must ration scarce resources. In market economies, price rations goods; in command economies, central planning/queues ration. - **Modern Economies and Mixed Systems:** Most real-world economies are mixed, combining elements of both market and command systems. Governments play a role in regulation, public goods provision, and income redistribution, while markets handle most production and distribution. - **Resource Allocation and Output/Income Distribution:** How resources are allocated (what is produced) directly impacts how output and income are distributed among the population. ### Production Possibilities Curve (PPC) - **Introducing the Model:** A graph showing the maximum possible output combinations of two goods or services an economy can achieve when all resources are fully and efficiently employed, given technology. - **Conditions for Maximum Output:** - Fixed amount of resources. - Fixed technology. - Full employment of resources. - Productive efficiency (producing on the curve). - **PPC and Scarcity, Choice, Opportunity Cost:** - **Scarcity:** Illustrated by points outside the curve (unachievable). - **Choice:** Moving along the curve represents choosing different combinations of goods. - **Opportunity Cost:** The negative slope of the PPC. To produce more of one good, less of the other must be produced. - **Shape of the PPC:** - Typically **concave to the origin** (bowed outwards). This reflects the Law of Increasing Opportunity Cost. As more of one good is produced, resources less suited for its production must be used, leading to higher opportunity costs. - A **straight line PPC** implies constant opportunity cost, meaning resources are perfectly adaptable between the production of two goods. - **Potential GDP and the PPC:** The PPC represents the economy's potential GDP – the maximum output when all resources are fully employed. - **Economic Growth and the PPC:** An **outward shift** of the PPC indicates economic growth, meaning the economy can produce more of both goods. - **Factors Leading to an Outward Shift of the PPC:** - Increase in quantity of resources (e.g., more labor, discovery of new natural resources). - Improvement in quality of resources (e.g., better education for labor). - Technological advancements (more efficient production methods). - **Maintaining Growth with Low Unemployment and Efficiency:** To realize potential growth, resources must be fully employed (low unemployment) and used efficiently (operating on the PPC). - **Efficiency, Sustainability and the PPC:** - **Productive Efficiency:** Operating on the PPC. - **Allocative Efficiency:** Producing the combination of goods most desired by society (a specific point on the PPC). - **Sustainability:** Producing in a way that meets current needs without compromising future generations' ability to meet their own needs. This can influence the long-term shape and position of the PPC. - **Concept of Economic Growth v/s Economic Development:** - **Economic Growth:** Quantitative increase in real GDP or national income over time (outward shift of PPC). - **Economic Development:** Qualitative and quantitative improvements in the standard of living, including factors like health, education, income distribution, and environmental quality. Broader concept than growth. ### The Law of Demand - **Law of Demand:** States that, *ceteris paribus* (all else being equal), there is an inverse relationship between the price of a good and the quantity demanded. As price increases, quantity demanded decreases; as price decreases, quantity demanded increases. - **Non-Price Determinants (Shifters of Demand Curve):** - **Income:** - **Normal Goods:** Demand increases with income. - **Inferior Goods:** Demand decreases with income. - **Tastes and Preferences:** Favorable changes increase demand. - **Price of Related Goods:** - **Substitutes:** Goods used in place of each other (e.g., tea & coffee). Price of substitute increases, demand for original good increases. - **Complements:** Goods consumed together (e.g., cars & petrol). Price of complement increases, demand for original good decreases. - **Expectations:** Future price or income expectations. - **Population/Number of Buyers:** More buyers increase market demand. - **Types of Goods (based on income & related goods):** - **Normal Goods:** YED > 0 - **Inferior Goods:** YED 0 - **Complementary Goods:** CED ### Elasticity of Demand - **Definition:** Measures the responsiveness of quantity demanded to a change in one of its determinants. #### Price Elasticity of Demand (PED) - **Definition:** Measures the responsiveness of quantity demanded to a change in the good's own price. $$PED = \frac{\%\Delta Q_d}{\%\Delta P}$$ - **PED and Its Range of Values:** (Absolute value is usually considered) - **Perfectly Inelastic (PED = 0):** Quantity demanded does not change at all with price changes (e.g., life-saving medicine). Vertical demand curve. - **Inelastic (0 1):** Quantity demanded changes proportionately more than price (e.g., luxury goods, goods with many substitutes). - **Perfectly Elastic (PED = $\infty$):** Consumers will buy an infinite amount at one price, but nothing at a slightly higher price. Horizontal demand curve (rare, theoretical). - **Practical Ranges of PED:** Generally, necessities have low PED, luxuries have high PED. - **Determinants of PED:** - **Availability of Substitutes:** More substitutes = higher PED. - **Necessity vs. Luxury:** Necessities = lower PED; Luxuries = higher PED. - **Proportion of Income Spent:** Larger proportion = higher PED. - **Time Horizon:** Longer time = higher PED (more time to find substitutes). - **Definition of the Market:** Narrowly defined market (e.g., "blue jeans") = higher PED than broadly defined market ("clothing"). - **Applications of PED:** - **Business Decisions:** Pricing strategies (e.g., a firm with elastic demand will lose significant revenue if prices are raised). - **Government Policy:** Taxation (e.g., taxes on inelastic goods generate more revenue with less impact on quantity). - **Impact of Price Controls:** Understanding effects of price ceilings/floors. #### Income Elasticity of Demand (YED) - **Definition:** Measures the responsiveness of quantity demanded to a change in consumer income. $$YED = \frac{\%\Delta Q_d}{\%\Delta \text{Income}}$$ - **Range of YED Values:** - **Normal Goods (YED > 0):** Demand increases as income increases. - **Necessities (0 1):** Demand increases more than proportionately with income. - **Inferior Goods (YED 0):** If price of B increases, demand for A increases. - **Complementary Goods (CED ### The Law of Supply - **Supply and Supply Curve:** - **Supply:** The quantity of a good or service that producers are willing and able to offer for sale at various prices during a specific period. - **Supply Curve:** A graphical representation showing the relationship between price and quantity supplied, *ceteris paribus*. It is typically upward-sloping. - **Law of Supply:** States that, *ceteris paribus*, there is a direct relationship between the price of a good and the quantity supplied. As price increases, quantity supplied increases; as price decreases, quantity supplied decreases. - **Non-Price Determinants of Supply (Shifters of Supply Curve):** - **Cost of Production:** - **Input Prices:** Increase in wages, raw materials = decrease in supply. - **Technology:** Improved technology = decrease in cost, increase in supply. - **Number of Sellers:** More sellers = increase in market supply. - **Expectations:** Future price expectations (e.g., if producers expect higher prices, they might hold back current supply). - **Government Policies:** - **Taxes:** Increase in taxes = decrease in supply. - **Subsidies:** Government payments to producers = increase in supply. - **Prices of Related Goods (in production):** - **Substitute in Production:** If the price of a good that can be produced with similar resources increases, producers might shift production to that good, decreasing supply of the original good. - **Complement in Production:** Goods produced together (e.g., beef and leather). Increase in price of one might increase supply of the other. - **How Economists Explain the Law of Supply?** - **Profit Motive:** Higher prices make production more profitable, incentivizing firms to supply more. - **Increasing Marginal Costs:** As production increases, the cost of producing additional units tends to rise (due to diminishing returns to variable inputs). Firms need a higher price to cover these higher marginal costs. ### Price Elasticity of Supply (PES) - **What is PES?** Measures the responsiveness of quantity supplied to a change in the good's own price. $$PES = \frac{\%\Delta Q_s}{\%\Delta P}$$ - **Normal PES Values:** (Always positive, as supply curve is upward sloping) - **Perfectly Inelastic (PES = 0):** Quantity supplied does not change with price (e.g., unique artwork, fixed capacity in very short run). Vertical supply curve. - **Inelastic (0 1):** Quantity supplied changes proportionately more than price. - **Perfectly Elastic (PES = $\infty$):** Producers supply any quantity at a specific price, but nothing at a lower price. Horizontal supply curve. - **Determinants of PES:** - **Time Horizon:** - **Momentary/Very Short Run:** Perfectly inelastic (producers cannot adjust output). - **Short Run:** Some inputs variable, some fixed; usually inelastic or unitary elastic. - **Long Run:** All inputs variable; usually elastic (firms can adjust capacity, enter/exit market). - **Mobility of Resources:** Easily movable resources = higher PES. - **Ability to Store Output:** Perishable goods = lower PES. Durable goods = higher PES. - **Spare Capacity:** More spare capacity = higher PES (can increase output easily). - **Production Lag:** Longer production process = lower PES. - **Number of Producers:** More producers = higher PES. - **Application of PES:** - **Government Policy:** Impact of taxes/subsidies on producers. - **Market Response to Price Changes:** Understanding how quickly and significantly producers can respond to price signals. - **Volatility of Prices:** Inelastic supply tends to lead to more volatile prices in response to demand shocks. ### Market Equilibrium - **Definition:** A state where quantity demanded equals quantity supplied at a specific price. There is no tendency for the price or quantity to change. - **Equilibrium Price:** The price at which QD = QS. - **Equilibrium Quantity:** The quantity at which QD = QS. - **Surplus (Excess Supply):** Occurs when price is above equilibrium, leading to QS > QD. Downward pressure on price. - **Shortage (Excess Demand):** Occurs when price is below equilibrium, leading to QD > QS. Upward pressure on price. - **Changes in Equilibrium:** Shifts in either the demand or supply curve (or both) will lead to a new equilibrium price and quantity. - Increase in Demand (rightward shift): P↑, Q↑ - Decrease in Demand (leftward shift): P↓, Q↓ - Increase in Supply (rightward shift): P↓, Q↑ - Decrease in Supply (leftward shift): P↑, Q↓